Our energy system needs to be secure, affordable, and sustainable. Balancing these three factors to achieve net-zero greenhouse gas emissions (GHG) is key to the energy transition. Today, we are facing multiple challenges.

Our energy system needs to be secure, affordable, and sustainable. Balancing these three factors to achieve net-zero greenhouse gas emissions (GHG) is key to a successful energy transition.

In 2021, the European Commission published its milestone Fit for 55 package designed to reduce the EU’s GHG emissions by 55% by 2030 and to put the Union firmly on-track for net-zero by 2050. A year later, as a response to the Russian war on Ukraine, the European Commission published REPowerEU. The plan adds to Fit for 55 by focusing on reducing energy consumption, diversifying energy supply, and accelerating renewable energy deployment.

Against this backdrop, renewable and low-carbon gases (i.e., hydrogen and biomethane) are key solutions towards a secure, affordable, and sustainable energy system. This is reflected in the European Commission’s ambition to produce 35 billion cubic meters (bcm) (370 TWh) of biomethane and 10 million tonnes (Mt) (333 TWh LHV) of renewable hydrogen domestically by 2030. Additionally, 10 Mt of hydrogen should be imported by 2030.[1],[2] Currently, both biomethane and renewable hydrogen production across the EU is very low: Only around 10% of the targeted biomethane volumes are produced today, while for green it is less than 1%. Substantial efforts are needed to rapidly scale up renewable and low-carbon gases to meet short-term diversification and long-term net-zero targets.

of global hydrogen output is produced with renewable energy

biomethane domestic production in the EU

Figure 1. Total greenhouse gas emissions trend, EU, 1990–2020

Decarbonisation of sectors that are difficult to electrify

While direct electrification can decarbonise many applications across sectors, renewable and low-carbon gases are needed as a sustainable feedstock, for high-temperature heat and for fuels with high energy density.

In the industry sector, renewable and low-carbon gases are needed to mitigate GHG emissions from high temperature heat processes and to replace fossil feedstocks. In the transport sector, hydrogen and biodiesel may become most important for heavy road transport and international shipping. Aviation will continue to use kerosene, but from biogenic or synthetic origin. In the buildings sector, the deployment of hybrid heat pumps, a combination of electric heat pumps and boilers running on renewable and low-carbon gases, has the potential to save up to €61 billion per year (excluding infrastructure costs).[3]

The large uptake of renewable gases and the integration of gas infrastructure is estimated to save 10% of direct CO2 emissions from the energy sector in between 2030 – 2050. Biomethane supports the decarbonisation of the methane system (3425 Mt of direct CO₂ emissions from natural gas are avoided over the timeframe 2030 – 2050) and reduces energy import dependency at the same time.

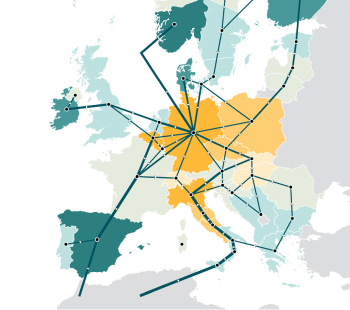

Assessing the benefits of a pan-European hydrogen transmission network

Integration of large shares of renewable electricity

The full decarbonisation of the energy system requires substantial quantities of renewable electricity. However, the intermittency of sun and wind brings the challenge to match electricity production with demand at a given time. A substantial volume of long-term, dispatchable energy storage will be needed.

Hydrogen and biomethane provide the optimal solution for dispatchable renewable electricity as they can be stored in large quantities, making it appealing for longer-duration storage. Gas-fired power plants running on renewable and low-carbon gases can be used to provide backup capacity during peak hours.

Integration of large shares of renewable electricity

Negative emissions are needed to compensate for the most hard-to-abate emissions in the future energy system. Biobased fuels such as biomethane combined with carbon capture and storage generate negative emissions. The ability to create negative emissions is significant because almost all authoritative climate change scenarios show that the world needs substantial negative emissions to achieve net-zero GHG emissions and keep global temperature increase well below 2°C

Hydrogen and biomethane provide the optimal solution for dispatchable renewable electricity as they can be stored in large quantities, making it appealing for longer-duration storage. Gas-fired power plants running on renewable and low-carbon gases can be used to provide backup capacity during peak hours.

Cost-effective energy transition

Biomethane and green hydrogen production costs will become increasingly competitive against natural gas and grey hydrogen with market scale-up and increasing EU ETS prices. This shows the potential of renewable gases in alleviating energy costs for consumers and companies. Regardless of natural gas prices, domestic renewable gas production should offer a more stable price outlook as these are not linked to the cyclical prices of fossil fuels and thus contribute to a better stability of the European energy market.

Moreover, the existing gas infrastructure can be repurposed or even used directly to transport large quantities of biomethane or hydrogen cost-effectively to provide dispatchable electricity. Pipelines can transport hydrogen at €0.11-0.21/kg (€3.3-6.3/MWh) per 1,000 km, outcompeting transport by ship for all reasonable distances within Europe and neighbouring regions.[4]

Hydrogen and biomethane provide the optimal solution for dispatchable renewable electricity as they can be stored in large quantities, making it appealing for longer-duration storage. Gas-fired power plants running on renewable and low-carbon gases can be used to provide backup capacity during peak hours.

Figure 2. Natural gas price developments compared to biomethane production costs

Figure 3. Hydrogen production costs

System cost savings

We estimate that the efficient use of renewable and low-carbon gases can lead to societal costs savings of up to €217 billion annually compared to a scenario that focuses on electrification only. The savings arise from lower costs for insulation and heating technologies in buildings (€61 billion), using hydrogen transported through gas infrastructure to decarbonise high temperature industrial heat (€70 billion), lower energy costs in transport (€14 billion), deployment of gas-fired dispatchable power as compared to more expensive solid biomass-fired dispatchable power (€54 billion) and efficient use of energy infrastructure (€19 billion). [5]

Use of renewable and low-carbon gases can lead up to

billion

societal costs savings

Sustainable agriculture

Biomethane strengthens the case for sustainable agriculture. Producing feedstocks with sequential cropping ensures that the soil is covered almost throughout the year, which reduces the need for synthetic fertiliser and increases earnings from the cropland. An increase in farmers’ revenues from biomethane production would improve their quality of life and their ability to invest.

Future-proof jobs

Most of the renewable and low-carbon gas demand can be satisfied with domestic production, meaning that jobs and value-added remain in the EU. Scaling up these gases is estimated to create 600,000-850,000 additional direct jobs and 1.1-1.5 million indirect jobs by 2050. [6]

Diversifying energy supply

Meeting the REPowerEU targets would result in reducing the EU’s dependency on natural gas imports by 30% by 2030.[7] Domestically produced biomethane used as a direct substitute of natural gas could replace around 12% of the 2021 natural gas imports by 2030.[8] The domestic production and imports of hydrogen can reduce EU dependency on fossil fuels further, e.g., hydrogen produced from natural gas can be replaced with hydrogen produced from renewable electricity.[9]

Reduce EU’s dependency on natural gas imports by

Europe has the potential to supply enough renewable gas to match the projected demand in 2050

In 2050, the domestic renewable hydrogen supply potential in the EU and UK is estimated to be 4,000 TWh which can sufficiently cover the demand of 2,300 TWh (2,150-2,750 TWh). This corresponds to 20-25% of EU and UK final energy consumption by 2050. [10]

On the biomethane potential, enough sustainable feedstocks are available in the EU-27 to meet the REPowerEU 2030 target of 35 bcm biomethane production. Our estimation shows that up to 41 bcm of biomethane in 2030 and 151 bcm in 2050 could be available. [11]

In 2050, renewable hydrogen covers 92-98% of hydrogen demand in our scenarios, the remainder is hydrogen produced from biomethane in combination with carbon capture – a technology that generates much needed negative emissions. Low-carbon hydrogen produced from natural gas is a transitional solution to kick-start the hydrogen economy and is phased out after 2040.[12]

The domestic renewable gases supply potential in the EU and UK in 2050

TWh hydrogen

biomethane

In the short- to mid-term, imports of hydrogen and derivatives play an important role

In addition to domestic (EU27, UK, Norway) hydrogen supply, abundant natural resources and geographic proximity drive the favourable economics of pipeline imports from neighbouring regions such as North Africa, and Ukraine, making these regions attractive partners for future hydrogen trade. Also, shipped imports of hydrogen and its derivatives such as ammonia play an important role and contribute to supply diversification.[13] To realise substantial amounts of hydrogen imports already by 2030, permitting of cross-border infrastructure needs to be simplified, common sustainability criteria for hydrogen production established, and financing mechanisms for international hydrogen projects put in place.[14]

Facilitating hydrogen imports from non-EU countries

Sustainable feedstocks need to be mobilised to scale-up biomethane production

To meet the 2030 35bcm biomethane production target, mobilisation of sustainable feedstocks needs to be prioritised. Waste and residue feedstocks including manure, agricultural residues, food waste, and industrial wastewater are the prime candidates for immediate activation. These feedstocks are cheapest and offer the highest GHG emissions savings. The European Commission should set out a clear and sustainable approach to using crops for biomethane. This approach should include appropriate definitions and guidance for the use of sequential cropping as part of sustainable farming practices.

Figure 4. Biomethane potential in 2030 per technology and country

Pan-European hydrogen transmission network generates €330 billion in cost savings

An interconnected European hydrogen network offers significant benefits already in 2030 and can connect demand clusters and regions with high renewable energy supply potentials in a cost-efficient way, saving €330 billion between 2030 and 2050. Hydrogen production is shifted to regions with more advantageous renewable resources, and on average, lower electricity prices. Due to the deployment of cross-border infrastructure, investments into electricity cross-border transmission and battery storage capacities are reduced significantly compared to a clustered scenario.

The European Hydrogen Backbone (EHB) initiative envisioned a pan-European hydrogen transmission system utilising existing gas infrastructures across 28 countries. Five hydrogen corridors can effectively accelerate the decarbonisation of our energy system while increasing energy security in the EU. Immediate actions need to be taken to ensure that the required infrastructure will be in place at the end of the current decade, such as ramping up electrolyser capacity and a rapid implementation of an enabling regulatory framework.[15]

European Hydrogen Backbone

Significant ramp-up of storage capacity for hydrogen

Large-scale storage for hydrogen will be a core component of the integrated European energy system. Hydrogen storage capacity requirements have been preliminarily estimated at around 70 TWh by 2030, with a growing storage needs of around 500 TWh in 2050.[16] However, current storage capacities are insufficient to meet hydrogen storage demand in 2030. New and repurposed storage infrastructure is needed to facilitate hydrogen imports.

Biomethane integration into the gas grid infrastructure

A scale-up of biomethane from 3 bcm to 35 bcm by 2030 requires significant integration into the gas grid infrastructure. Recommended actions to facilitate the integration include updating the quality standard for cross-border gas, identifying projects to pool multiple sources of biogas to a central upgrading biomethane plant, minimising connection and grid integration costs, and implementing regional mapping (zoning) of potential biomethane production in all Member States.

Assessing the benefits of a pan-European hydrogen transmission network

Manual for national biomethane strategies

Gas for Climate webinar – Assessing the benefits of a pan-European hydrogen transmission network

Renewable gas can be massively scaled up by 2050. Biomethane should be allocated based on the highest societal value. Hydrogen will be used in hard-to-decarbonise sectors – in industry as feedstock and for high-temperature heating, in the building sector, in power system balancing on long-time scales (e.g. hydrogen peaking plants), and in mobility applications, either as hydrogen or hydrogen-based synthetic fuel (aviation, maritime, heavy-trucking). Hydrogen is a prime candidate to facilitate sector coupling and fits well into the efforts for increased electrification by providing long-term storage and possibly also dispatchable power generation.

A substantial part of the current gas imports from Russia (155 bcm in 2021) can be replaced by domestic biomethane production (35 bcm) and renewable hydrogen production and import (50 bcm) by 2030. At the European level, supply potential is sufficient to meet the demand for renewable gases at all time scales (2030, 2040, and 2050), subject to acceleration of Renewable Energy Sources (RES) build-out beyond current targets. Individual regions might experience an abundance or lack of sufficient renewable energy and accelerated development of the European Hydrogen Backbone will help reconcile these differences can help to reconcile these differences.

Gas for Climate fully supports the Fit for 55 package, aimed at a 55% reduction in European emissions by 2030 and the accelerated goals under REPowerEU. Gas for Climate also promotes a target 35 bcm of biomethane and 20 Mt of hydrogen in the European Union by 2030. Scaling up of renewable hydrogen (deployment of electrolysis) and biomethane (driven in large by sequential cropping) production is possible. Renewable gases are the solution in removing barriers to decarbonisation and creating the conditions for a more cost-effective transition. Policymakers are to adapt the European Union’s regulatory framework so that the production of renewable and low-carbon gases is incentivised, and gas infrastructure can fully unleash its great potential in a future integrated energy system.